The Importance of Credit Score in the Indian Lending Industry

In today’s scenario buying things on credit is a common phenomenon, some of the biggest purchases like a house or some small purchases like consumer durable products are backed by loans. Hence creditworthiness plays a crucial role in an individual's life. Good and bad credit score in India, are two distinct terms that define an individual's ability to borrow and access favourable loan terms. In this article, we will explore the importance of credit ratings in the Indian lending industry, examine key statistics regarding good vs bad credit scores in India, and emphasize the idea that taking a loans like loan against mutual funds and shares is not inherently a bad thing.

What is Credit Score?

A credit score is a three-digit number that summarizes your credit history. Lenders use it to assess your creditworthiness or the likelihood that you will repay loans in a timely manner. The higher your credit score, the more likely you are to be approved for loans and for better interest rates. You can improve your credit score by making all your payments on time, keeping your debt levels low, and opening and using credit accounts responsibly.

Understanding Good Credit Scores vs Bad Credit Scores:

Creditworthiness is evaluated based on an individual's credit history, which reflects their past borrowing behaviour and repayment patterns. Good credit score refers to a positive credit history, where borrowers have a track record of making timely payments, managing debts responsibly, and maintaining a low credit utilization ratio. On the other hand, bad credit score indicates a negative credit history, characterized by missed payments, defaults, high credit utilization, and other financial missteps.

Statistics on Good Credit Scores vs Bad Credit Score in the Indian Lending Industry:

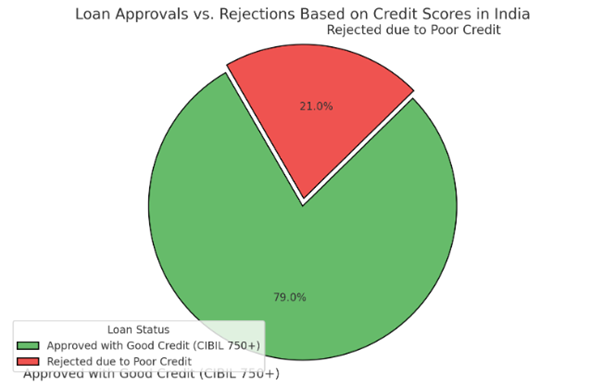

Lenders rely on various credit information companies (also known as credit bureaus or credit reporting agencies) to collect and maintain credit information of individuals. According to recent data from the Credit Information Bureau of India Limited (CIBIL), a leading credit bureau in India, around 79% of loans approved by banks in the country are for individuals with a CIBIL score of 750 or above, indicating good credit.

This demonstrates that a strong credit profile significantly enhances the chances of loan approval and favourable interest rates. In contrast, borrowers with bad credit face challenges as lenders perceive them as higher risk. It is estimated that around 21% of loan applications are rejected due to poor credit scores, making it essential for individuals to maintain a good credit history.

Taking a Loan: Not a Bad Thing:

Contrary to common misconceptions, taking a loan is not inherently a bad thing. In fact, responsible borrowing can be a valuable financial tool that helps individuals achieve their goals, whether it's purchasing a home, financing education, or starting a business. Loans provide the necessary funds to bridge the gap between income and expenses, empowering individuals to pursue opportunities that may not be feasible otherwise. It is crucial, however, to borrow within one's means and make consistent, on-time repayments to maintain a good credit score.

How to maintain a Good Credit Score?

When it comes to maintaining a good credit score one should follow the below practices.

1). Paying EMIs & Loans on Time:

Any default or missed payment affects the credit score. Timely repayments & paying with credit card balance in full every month helps improve the credit score.

2). Healthy Credit Mix:

An ideal credit mix includes a blend of revolving and instalment credit. A credit card for which you make monthly payments and no particular end date unless you close the account is a revolving credit. A car loan for which you make fixed payments monthly and has a specific end date is instalment credit. Having both revolving and instalment credit makes for a perfect duo because the two demonstrate your ability to manage different types of debt.

3). Credit Utilisation:

Credit utilisation means how much credit you use out of your available credit. An ideal utilization rate is around 30%.

Example Illustrating Good Credit Score vs Bad Credit Score:

Let's consider the example of two individuals, Ravi and Meera, both seeking a car loan. Ravi has a good credit history, reflected by his consistent bill payments, low credit card balances, and a favourable credit score of 800. Due to his reliable creditworthiness, Ravi qualifies for a car loan with a competitive interest rate and favourable repayment terms.

In contrast, Meera has a history of missed credit card payments and a high credit utilization ratio. Her credit score stands at 550, categorizing her as having a bad credit score. As a result, Meera faces difficulties in securing a car loan and may be offered less favourable terms or higher interest rates, if approved.

Conclusion:

In the Indian lending industry, a good credit score is a valuable asset that opens doors to financial opportunities, including lower interest rates, higher loan amounts, and faster approvals. It is crucial for individuals to recognize the significance of maintaining a positive credit history by making timely payments and managing debts responsibly. While a bad credit score may present challenges, it is not a permanent barrier. With consistent efforts to improve creditworthiness, individuals can rebuild their credit profiles and gain access to more favourable lending options.

Remember, taking a loan is a responsible financial decision when done prudently and can help individuals achieve their dreams and aspirations. It is also recommended to opt for an honest and transparent lender who can provide thorough explanations of all associated expenses and procedures, as well as offer guidance during challenging circumstances.